Table of Contents

Introduction.

Homeowners’ insurance policies may provide coverage for furnace repairs or replacement, but it depends on the policy and the cause of damage. Standard policies typically cover damage caused by fire, wind, hail, and other perils. This includes electrical breakdowns and mechanical problems from wear and tear. To cover furnace repairs or replacement, some policies may require additional coverage for mechanical breakdowns or equipment breakdowns. Read your homeowners’ insurance policy to understand what is covered and what is not covered. State Farm does not offer coverage for boilers or furnaces in their standard policies. However, they do offer optional add-ons like Home Systems Protection, which covers up to $50K for HVAC issues. Other companies, such as Lemonade, also offer optional protection plans for appliances like air conditioning units. Keep your equipment in shape with regular service and inspections.

Homeowners Insurance Coverage For Furnace.

To ensure your furnace is covered in case of damage or breakdowns, homeowners insurance is the way to go.

When it comes to homeowners insurance, coverage for your furnace depends on your specific policy, as well as factors like your furnace’s age and the cause of damage.

In this section, we’ll discuss different types of homeowners insurance policies that cover furnace repairs or replacements.

We’ll also explore add-on coverage options for additional protection, such as equipment breakdown coverage and mechanical breakdown coverage.

Standard Homeowners Insurance Policies.

Homeowners Insurance offers coverage for structural damage, personal property, liability,y protection, and extra living expenses. These policies don’t include every loss or damage category, so make sure that your coverage meets your needs.

Coverage for a furnace might be subject to certain conditions or limitations that depend on the policy.

If it’s damaged by a covered hazard, like fire or hail storm, then it could be covered under some policies. But if it breaks down due to wear and tear or neglect, it might not be covered. Read your policy carefully to understand what is and isn’t covered in case of furnace breakdowns.

You need to know about all the coverages available in homeowners’ insurance policies.

These policies differ depending on the client’s needs and the states they live in.

So, always confirm whether you have replacement cost or actual cash value coverage when you buy an insurance policy.

The Balance (2021) states that “If someone gets hurt while visiting your home with your permission, this part of your homeowners’ insurance will help pay their medical bills and other costs if they file a claim”.

If your furnace is crucial for your home, then dwelling coverage keeps it running.

Dwelling Coverage.

Property damage coverage safeguards the structure of your crib, including the furnace. It covers destruction from disasters like fire, hail, or windstorms. The extent of the coverage is determined by the policy limit.

It’s important to check if you’ve got enough coverage in case of damage so that you can safeguard yourself from costly repairs. Recall to review and renew your policy consistently.

Pro Tip: Stay on top of regular maintenance for your furnace to avoid potential damages which could result in denied claims.

Furnace catchin’ fire? Don’t worry, your homeowners’ insurance will step up and take care of that blaze.

Covered Loss.

Homeowner’s insurance policies cover certain risks related to the main house of the insured.

For furnaces, the coverage varies depending on what caused the damage, the type of policy bought, and other elements.

Here’s a table showing the usually covered losses for a furnace under homeowners’ insurance policies:

| Perils/risks | Coverage |

| Fire/Explosion | Yes |

| Theft | No (need separate policy) |

| Flood/Water Damage | No (need separate policy) |

| Mold/Bacteria Growth | No (unless from covered peril) |

It’s important to remember that, usually, normal wear and tear or mechanical breakdowns are not included in homeowners’ insurance policies. But, some insurers provide extra options to cover those costs.

For complex claims, policyholders may need to collaborate with a licensed public adjuster or HVAC expert to investigate and show damages before filing a claim.

The National Association of Insurance Commissioners did a study and found that furnace-related claims made up about 6% of all homeowners’ insurance claims filed in the US in 2019.

If only our furnace was covered like our couch, it could provide warmth; instead of us freezing!

Lack of Coverage.

Homeowner’s insurance may cover some losses due to furnace-related damage. But, certain policy clauses or conditions may stop you from getting compensation.

Normal wear and tear, lack of maintenance, or self-inflicted damage is usually not included in a standard policy. Earthquakes, floods, surges, or nuclear hazards may also need extra protection.

Read your policy documents carefully. Make sure you know the terms and limitations of furnace repair or replacement. In some cases, you may need special riders or endorsements for more coverage.

John had a gas furnace installed in his basement. It started leaking carbon monoxide one winter day. He called a repair technician, who found out that an unlicensed contractor did the faulty work. The repair cost was $2000, but John’s insurer denied his claim, due to his policy exclusion of damages from unlicensed contractors.

In conclusion, homeowners insurance can help with unexpected furnace failures due to covered perils like fire, lightning strikes, or theft. But, check with your agent about what your policy protects. Make sure you are prepared to fill any gaps in your coverage.

Keep your furnace covered, so you won’t be left in the cold (or with a massive repair bill).

Additional Coverage for Furnace.

Protecting your furnace is essential for homeowners who want to make sure they’re covered in the event of damages.

Here’s the deal on extra insurance for this important appliance.

| Coverage | What It Protects |

| Equipment Breakdown | Fixes or new costs due to mechanical, electrical, or pressure-related problems. |

| Home Systems | Security for heating and cooling systems, including furnaces. |

| Water Damage | Guards against water damage caused by a malfunctioning furnace, like burst pipes. |

It’s worth noting that not all homeowners insurance policies cover furnace damages. To be covered, you must get the right coverage ahead of time.

Homeowners can pick from various plans based on their budget and needs. The level of protection needed will depend on factors such as location, age of the appliance, and weather conditions.

For example, one homeowner whose furnace broke down was able to file an equipment breakdown claim with her insurance company. The policy paid for a new furnace and installation. Without this extra coverage, she’d have been stuck with a costly bill for these surprise repairs.

That’s why homeowners need to check out the different types of coverage available and pick the ones which best protect their property investment over time.

Mechanical Breakdown.

Homeowners’ insurance coverage for furnaces offers protection against mechanical failures. This coverage usually includes motors, blowers, and fans. The insurance may cover repair or replacement costs if they break down due to wear and tear or other malfunctions.

It is important to review the policy carefully, as some may have exclusions or limits. Regular maintenance and inspections can help prevent mechanical failures and keep the furnace running.

Having homeowners insurance coverage for furnace mechanical breakdowns can give peace of mind knowing costly repairs are covered.

So, be sure to check your policy and protect your wallet.

Equipment Breakdown Coverage.

Equipment Failure Coverage is an essential part of Homeowners Insurance. It’s there for your furnace and other major appliances, protecting them from unexpected breakdowns and damages.

Repair Costs? Covered. Replacement Costs? Got it. Legal Fees? Yes, those too!

However, keep in mind that Equipment Failure Coverage usually doesn’t cover regular wear and tear or damages caused by poor maintenance. So, make sure you maintain your furnace to keep it running for longer.

It’s important to read the terms and conditions of your policy carefully, so you know what is covered in case of a claim.

That way, you’re not surprised when filing a claim.

When And What Furnace Damage Is Covered In Homeowners Insurance Coverage.

To understand if and when your furnace damage is covered by your homeowners’ insurance policy, here’s what you need to know.

In this section, we will discuss the reasons behind furnace damage and the costs that your insurance policy may cover for furnace repairs and replacements.

Causes of Furnace Damage.

Furnace destruction can have many causes.

- Factors like neglected maintenance, wear, and tear, and mistakes by operators are potential contributors.

- Outdated air ductwork systems can also cause harm.

- Electrical wiring or gas leaks near the furnace may create serious damage.

Protection of your furnace is key. Choosing the correct-sized air filter for your HVAC and replacing it regularly is a good preventive measure.

It’s important to keep all furnace components clean and well-maintained.

When there’s a major appliance repair issue, always hire a qualified repair service to inspect the problem and take preventive steps.

Harvard University states that solar panels generate 90% fewer carbon emissions than coal-powered energy sources.

Caring for your furnace is important, but at least you don’t need an oil change.

Mechanical Problems.

Mechanical issues can mess up a furnace. This can lead to extra costs.

Here are some common mechanical problems:

- A blocked or dirty air filter restricts airflow and increases energy consumption.

- A blower motor that stops working leads to no airflow.

- A faulty ignition system can cause stoppage or gas leakage. This is a health hazard.

It’s important to read the manufacturer’s warranty to know which components are covered.

Pro Tip: Do regular maintenance checks to identify issues before they become expensive repairs.

If you experience accidental damage, make sure you’re prepared!

Accidental Damage.

Furnace mishaps are no joke; but are you covered? Accidents can range from dents to more serious issues like water or fire damage.

- Many insurance policies cover sudden catastrophes that affect the indoor mechanisms of your furnace.

- Check the limited scope of the policy before signing any contracts.

- Don’t miss out on securing peace of mind!

And don’t forget to ask if water damage is covered; it’s important to know!

Water Damage.

Water damage to your furnace can cause big problems!

- Rust and corrosion can occur if any water gets inside.

- As a homeowner, you should know what counts as water damage and whether your insurance will cover it.

- Look for condensation or water pooling around the furnace.

- Rust or corrosion on the unit could mean water damage.

- If you spot these signs, contact a pro right away.

Standard insurance policies may not cover water damage from floods or appliances like furnaces. But, sudden leaks not from long-term neglect may be covered. Check with your provider to be sure.

Be proactive and protect your furnace! Don’t wait for damage to happen.

Ask your agent about insurance coverage today; before your furnace shakes things up!

Earthquake Damage.

Natural Disaster Damage.

Is furnace damage from natural disasters, like earthquakes, covered by the warranty? It depends.

The specific language of the warranty and the kind of damage incurred are key factors.

In most cases, earthquake-caused damage is not covered. Though, if you purchased extra coverage, or live in an earthquake-prone area, you may be in luck.

It is important to review your furnace warranty closely and take note of any additional coverage options. That way, you’ll know what natural disaster damage is covered.

It’s staggering: The National Earthquake Information Center reports that the US alone experiences around 5,000 earthquakes each year.

Fire Damage.

Furnace damage due to fire can be a frightening experience for homeowners. Thankfully, most insurance policies cover this type of damage, but certain requirements must be met.

- It must be proven that the fire was unintentional and happened suddenly, as well as proof of ownership or possession at the time of the incident.

- Documentation of any lost belongings should be provided to assess compensation.

- However, some exclusions may apply depending on the insurer’s guidelines. This could include intentional fires or damage caused by natural events such as floods or earthquakes.

- To minimize any potential losses, regular maintenance and inspections of your furnace are vital.

It is also wise to repair any damages promptly.

Electrical Breakdown.

Electrical Malfunctioning.

Unexpected electrical issues can damage your furnace. This is usually covered by homeowners’ insurance policies.

- Malfunctions can be in the motor, blower, or circuits. It can cause odors or noises from the furnace.

- Insurance usually covers repair costs for technical failure and power surge situations. But, it doesn’t apply if the electrical issue was due to wrong installation or lack of maintenance.

- You must hire licensed professionals to repair within set time frames.

- In some cases, insurance may give money to replace the furnace due to electrical issues; but only if it meets certain criteria.

- It doesn’t cover just replacing an old system that isn’t working.

If a homeowner’s child tinkers with the thermostat, causing the HVAC system to overheat, it won’t be covered. This counts as intentional and personal damage.

Choose between a new furnace or a tropical holiday. A tan won’t keep you warm at night!

Cost Coverage for Furnace Repair and Replacement.

When your furnace stops working, you may worry about the repair or replacement costs.

- It depends on the cause of damage, your insurance policy, and any warranties. Homeowner’s insurance and manufacturer’s warranties can cover furnace repairs or replacements.

- You must check what each policy covers and talk with relevant people. Also, preventive maintenance can help avoid costly damages.

- Insurance policies can cover repair costs or just replacement expenses. If the damage is caused by negligence or lack of maintenance, insurers may not provide coverage.

A faulty furnace can be dangerous and cause serious damage if it is not fixed by professionals.

Research says 30% of US homeowner claims are due to heating system problems, (Insurance Information Institute).

So, repair costs can be like a leaky faucet, always dripping!

Repair Costs.

The cost of repairing furnace damage can vary, depending on the type and severity.

Here’s a summary of the estimated costs:

| Repairs Needed | Estimated Cost |

| Thermostat Replacement | $100 – $300 |

| Electrical Issues | $200 – $800 |

| Pilot Light Repair/Replacement | $150 – $400 |

It’s important to check your insurance policy to see what is covered, as some repairs may not be included.

Most policies cover furnace damage caused by unforeseen events like fire, hail, or wind. However, damages due to neglect or normal wear and tear may not be covered.

A study showed that most households don’t get their furnaces checked regularly. But regular maintenance can help you avoid expensive repairs and ensure optimal furnace performance.

So, if you don’t want to spend more on repairs than your annual vacation, it might be time to say goodbye to your furnace!

Furnace Replacement.

Replace Broken Furnace.

- When your furnace is damaged, you may need to replace it.

- Insurance coverage can determine how much you pay.

- The extent and cause of damage decide if you get new equipment or repairs.

- The age of the furnace is relevant too. If it’s too old, it may not be covered. Usually, the insurance company pays for installation.

But, check the policy first!

Pro Tip: Establish safety protocols and obtain permits from local authorities before buying or installing a new furnace.

If you have homeowners insurance, you need to prove that the furnace exploding was not your fault to get coverage.

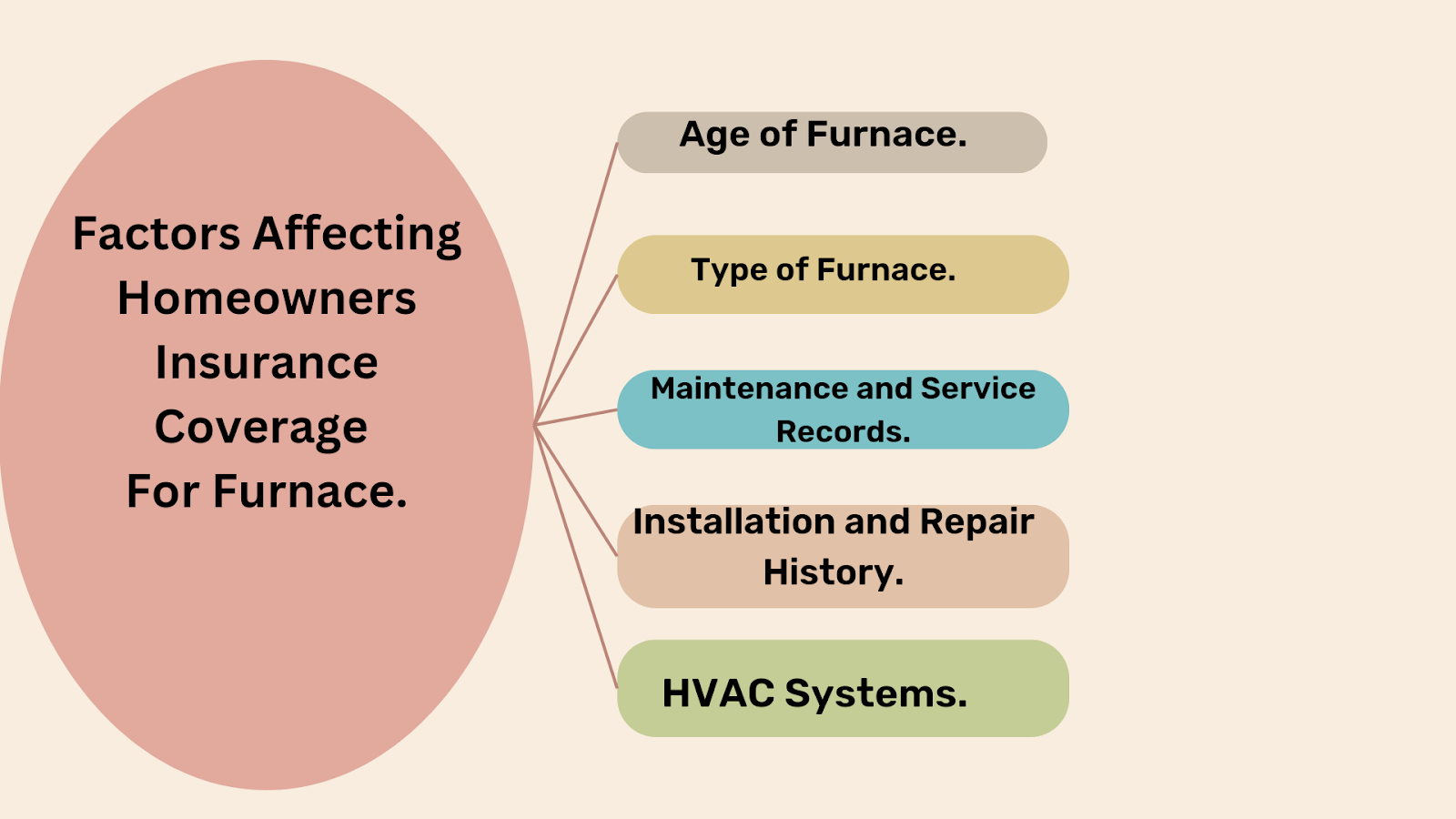

Factors Affecting Homeowners Insurance Coverage For Furnace.

To ensure you have proper homeowners insurance coverage for your furnace, you need to consider several factors.

To manage the risk associated with your furnace, the age of the furnace, type, and many other issues must be accounted for.

Through a detailed examination of these factors, you can make the most informed decisions on your coverage plan.

Age of Furnace.

The age of your heating system is a major factor in how much insurance coverage you can get for it.

- As your furnace gets older, it becomes less efficient and more likely to break down or completely fail. Insurers take the age of the furnace into account when setting rates.

- Aside from age, maintenance, and servicing frequency are also important. Regular maintenance can prolong the furnace’s lifespan and reduce the chances of breakdowns. Those who keep up with maintenance tend to get better coverage.

- For optimal protection, professional inspections should be done regularly.

- These can spot potential problems early and prevent bigger issues in the future. Plus, timely maintenance makes you eligible for better insurance policies.

No one wants to lose money in case of unexpected failures or breakdowns. To prevent this, make sure your furnace gets the care it needs throughout its life.

So don’t forget to schedule those regular inspections!

Type of Furnace.

Furnace Type is a crucial factor in Homeowners Insurance Coverage.

It can make a huge difference in the insurance policy as it decides the amount of risk or loss.

The table can be crafted to show different Furnace Types and their effect on insurance coverage. The columns should include Furnace Type, Risk Assessment, and Premium Amount. A Gas Furnace, for instance, may have a moderate risk assessment but a lower premium than an Oil Furnace with a higher risk assessment.

Other details that can influence insurance coverage are the age and condition of the furnace and its maintenance history.

It’s important to tell the insurance provider about any upgrades done to the furnace system for proper coverage.

Insure.com states: “Homeowners policies generally cover collapsed furnaces due to issues such as rusted heat exchangers and from cold weather-related causes.” It is essential to inspect policy details and get extra coverage if required.

Be sure to keep your furnace service and maintenance records up-to-date, or you’ll be stuck in the dark with your insurance company cashing in.

Maintenance and Service Records.

For comprehensive homeowners insurance coverage of your furnace, it’s critical to keep meticulous records of all maintenance and servicing activities.

Keeping track of all scheduled services and preventive maintenance not only proves regular upkeep but also serves as proof of proper care in case of damage or loss.

The table below lists the key elements to be included in your maintenance and service records:

| Maintenance Activity | Date | Contractor/Technician Name | Work Performed |

| Annual Furnace Tune-up | 01/16/2021 | ABC Heating & Cooling | Cleaned Burners, Checked Electrical Connections, Inspected Filters, etc. |

| Filters changed | 03/15/2021 | Self-service | One-year air filter. |

| Thermostat Checkup | 04/12/2021 | XYZ Furnaces | Adjust thermostat settings. |

Also, having all invoices in order can be valuable at the time of filing claims.

With such records at hand, it may prevent any disputes about coverage between homeowners and insurers.

Pro Tip: Don’t skip annual heating system inspections and keep a file for all records of maintenance or servicing work to ensure optimal coverage for your furnace.

Your furnace’s installation and repair history should be top-notch; otherwise, insurers won’t be interested.

Installation and Repair History.

For proper homeowners insurance coverage, it’s important to look into the history of installation and repair.

How often the furnace is maintained and repaired is key for understanding damage-prone areas. A good maintenance record shows care was taken.

Look at this table to better understand what to look for when assessing the installation and repair history to determine furnace system coverage:

| Date | Repair Type | Service Provider Name |

| Jan | Pilot Light Repair | Best Home Services Inc. |

| Jul | Wiring Replacement | JJ’s Heating and Cooling |

| Nov | Heat Exchanger Replacement | John’s HVAC Systems |

Insurance providers need data from check-ups, maintenance records, and repairs to assess risk for furnaces. Replacement or updates on parts (like heat exchanger, pilot light, and wiring) must be installed as per safety regulations.

According to The Insurance Information Institute, damages caused by furnaces cost around $4.7 billion a year in property losses.

In conclusion, looking at an installation & repair history helps reduce risks associated with damage-prone areas. That way, you can better predict future breakages resulting in damage costs.

But if the worst happens and your HVAC system fails, remember that insurance won’t cover you huddling around a flaming pile of rejected claims!

HVAC Systems.

- Climate control systems in a dwelling are important for comfort.

- Age, type, and condition of HVAC systems can affect homeowners’ insurance premiums. Providers may consider inspections, maintenance schedules, and upgrades when they are underwriting policies.

- Certified professionals should inspect HVAC systems often to make sure they are working well.

- Quality of installation and design is necessary for furnaces.

- Insulation to stop heat loss is also important for policy premiums.

- Upgrading or replacing aged and inefficient HVAC equipment can result in lower premiums due to increased reliability and efficiency.

- Smart thermostats can provide better control over energy use, leading to discounts.

Insurance companies love your furnace, but if it gets worn down, they won’t be so happy!

Homeowners Insurance Companies And Furnace Coverage.

To ensure proper coverage for your furnace, it’s important to understand how your homeowners’ insurance policy works.

If your furnace breaks down or suffers damage, you need to figure out if your policy covers the repair costs or replacement.

In this section, we’ll guide you through the limits on coverage, specific policy language, and homeowner insurance claim process for the furnace.

This information will provide valuable insight and help you make a more informed decision when it comes to protecting your home and appliances.

Limits on Coverage.

Limits of Insurance Coverage.

Understand the limits of your insurance coverage! It may not cover all furnace-related issues and losses.

Check out the table below for common homeowner insurance policies and their coverage limits:

| Type of Policy | Coverage Limit |

| HO-1 | Limited Coverage |

| HO-2 | Named Perils Only |

| HO-3 | All Risk Policies, excluding certain named perils |

| HO-4 | Renter’s Insurance, personal belongings only |

| HO-5 | Condominium Insurance |

Be sure to read through your policy documents. Know that each policy has exclusions and some forms of damage or loss may not be covered.

The top five homeowner insurance companies according to JD Power are:

- State Farm.

- Amica Mutual.

- Auto-Owners Insurance.

- Erie Insurance.

- Nationwide.

Your insurance policy may be written in English, but when it comes to furnace coverage, it could be alien speak!

Specific Policy Language.

When it comes to homeowners insurance and furnace coverage, there are key terms to be aware of.

Deductibles, limits, and exclusions all come into play.

- Deductibles are the amount you must pay before insurance kicks in.

- Limits are the max amount the company will cover for damages.

- Exclusions include damage from lack of maintenance and normal wear & tear, as well as intentional or criminal acts.

It’s important to keep in mind that individual policies may come with unique details. For example, some may require proof of annual maintenance for coverage to apply.

Furnaces weren’t always included in homeowner policies. But, as technology advanced, the risk of fire damage decreased and furnaces became standard features in homes.

Consequently, most policies now cover furnaces under their ‘dwelling protection’ category.

Knowing furnace coverage policy language is essential for homeowners seeking to safeguard their investment and financial security in case of an incident.

So, don’t fear – filing a furnace claim with your homeowners’ insurance is easier than getting your teen to stay in on a Friday night!

Homeowner Insurance Claim Process for Furnace.

Furnace coverage is a must-have in any homeowner’s insurance policy.

The process for filing a claim is easy: just reach out to the insurance company and wait for them to assess the damage. After that, they’ll pay for repairs or replacement according to the policy’s terms.

However, it’s essential to check your policy’s limits on furnace coverage. You might need extra coverage for your furnace. Make sure to read and understand the policy before filing a claim.

In case of any disputes regarding a furnace coverage claim, you can get help from independent adjusters or property damage lawyers.

Bottom line: Homeowners insurance coverage for furnaces is like a warm blanket; it’s comforting to have, but you hope you never need it.

Frequently Asked Questions.

Q: Does homeowners insurance typically cover furnace repairs or replacements?

A: In most cases, homeowners insurance does not cover regular wear and tear or mechanical breakdowns of a furnace. However, if the damage to the furnace is caused by a covered peril, such as a fire or a burst pipe, it may be covered under your homeowners’ insurance policy.

Q: What types of perils or events are typically covered by homeowners insurance for furnace damage?

A: Homeowner’s insurance policies commonly cover perils like fire, lightning strikes, windstorms, hail, explosions, and water damage from a sudden and accidental source. If your furnace is damaged due to any of these covered perils, you may be eligible for reimbursement or coverage for repairs or replacements.

Q: Are there any specific exclusions related to furnace coverage in homeowners insurance?

A: Yes, certain exclusions may apply to furnace coverage. For example, damage resulting from lack of maintenance, normal wear, and tear, or negligence may not be covered. It’s important to review your policy or consult with your insurance provider to understand the specific exclusions and limitations related to furnace coverage.

Q: Can homeowners insurance cover furnace damage caused by a power outage or power surge?

A: Coverage for power outages or power surges that result in furnace damage may vary depending on your policy. Some homeowners insurance policies offer coverage for power surge-related damages, while others may require an additional endorsement or separate coverage. Review your policy or consult with your insurance provider to determine if such coverage is included or available.

Q: Does homeowners insurance cover the cost of routine furnace maintenance or inspections?

A: Homeowners’ insurance typically does not cover routine furnace maintenance or inspections. These are considered part of the regular upkeep and maintenance responsibilities of a homeowner. It’s advisable to refer to your policy documents or contact your insurance provider to confirm if any specific maintenance-related coverage is provided.

Q: Is it necessary to have additional coverage or a separate home warranty for comprehensive furnace protection?

A: While homeowners insurance may provide coverage for furnace damage caused by covered perils, it is often limited in scope. Considerations for additional coverage, such as a home warranty, may provide more comprehensive protection against mechanical failures, breakdowns, and other non-covered perils. Evaluate your specific needs and consult with insurance providers to explore suitable options for extended furnace coverage.

Conclusion

Homeowners’ insurance policies often provide coverage for furnace repairs or replacements due to certain damages. This includes fire, earthquakes, water damage, and more. However, limitations and exclusions may be present based on the age of the furnace and pre-existing conditions. Specific equipment breakdown coverage is also available for heating systems against appliance breakdowns or electrical failure. The age of the unit, cost of replacement, installation issues, and maintenance records are some factors that influence claims related to furnace damage. Insurance companies may also limit coverage based on dwelling coverage limits.